: Revolutionizing Security and Efficiency in Healthcare")

Polyester fiber, the workhorse of the modern textile industry, continues to dominate the global synthetic fiber landscape. Born from petrochemicals, its journey from a functional alternative to a versatile powerhouse reflects broader economic, environmental, and technological shifts. Today, the polyester fiber market is not just about volume; it’s navigating a complex web of sustainability challenges, innovation drives, and shifting geopolitical currents. This article explores the key trends, drivers, and future prospects of this indispensable market.

Market Overview: A Colossus Built on Scale and Cost

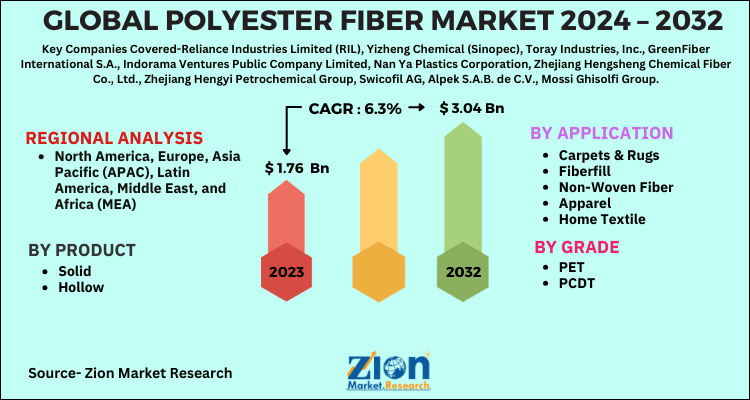

Polyester accounts for over 50% of the total global fiber production, a share that has steadily increased for decades. Its supremacy is built on a compelling value proposition:

-

Cost-Effectiveness: Significantly cheaper to produce than natural fibers like cotton or wool.

-

Durability & Performance: Renowned for strength, wrinkle resistance, quick-drying properties, and ease of care.

-

Versatility: Used across apparel (from fast fashion to sportswear), home textiles (bedding, upholstery), and increasingly in industrial applications (tires, conveyor belts, geotextiles).

-

Supply Chain Security: Unlike agriculture-dependent fibers, its production is less vulnerable to weather and seasonal fluctuations.

The Asia-Pacific region, led by China, India, and Southeast Asia, is the epicenter of both production and consumption, housing integrated petrochemical-to-fiber manufacturing complexes that deliver unmatched economies of scale.

Key Drivers Fueling Growth

-

Fast Fashion & Urbanization: The relentless pace of fast fashion demands affordable, adaptable, and durable materials. Coupled with rising disposable incomes and urban lifestyles in developing economies, this fuels continuous demand.

-

Performance Apparel Boom: The surge in athleisure, sportswear, and outdoor clothing relies heavily on advanced polyester variants (microfiber, moisture-wicking, thermal regulation).

-

Non-Woven & Technical Textiles: This is the fastest-growing segment. Polyester’s use in hygiene products, medical textiles, automotive interiors, and construction materials provides a stable, high-value demand stream.

-

Recycled Polyester (rPET) Momentum: Driven by brand commitments (e.g., Adidas, Patagonia) and regulatory pressure, rPET from post-consumer PET bottles is becoming mainstream. It offers a tangible path to circularity, though challenges in mechanical recycling quality and scale remain.

Challenges and Headwinds

The market faces significant pressure points:

-

Environmental Scrutiny: Polyester’s dependence on fossil fuels and the issue of microplastic shedding are major concerns. The industry is under immense pressure to decarbonize and address end-of-life issues.

-

Volatile Raw Material Prices: Linked to crude oil and PX (paraxylene) prices, profitability can be highly volatile.

-

Overcapacity & Trade Tensions: Periodic oversupply, particularly from China, depresses prices. Geopolitical tensions and shifting trade policies disrupt established supply chains.

-

Competition from Alternative Materials: While still niche, bio-based alternatives (PLA fibers) and renewed interest in natural fibers with better sustainability credentials present long-term competitive threats.

The Sustainability Imperative: Recycling and Innovation

The future of polyester is inextricably linked to its green transformation. Key initiatives include:

-

Mechanical Recycling: Well-established for bottle-to-fiber applications, but often leads to quality degradation (“downcycling”).

-

Chemical Recycling: Emerging technologies (e.g., depolymerization) that break polyester back to its monomers (PTA and MEG) promise fiber-to-fiber recycling with virgin-like quality. This is the holy grail for a circular polyester economy but needs scaling and cost reduction.

-

Bio-based Polyester: Developing routes to create PTA from biomass (e.g., sugarcane) is an active R&D area, aiming to reduce carbon footprint.

Future Outlook: A Market in Transition

The polyester fiber market is projected to continue growing, but its character is changing:

-

Dual-Track Growth: Virgin polyester will continue to grow in developing regions and technical applications, while recycled polyester will see explosive growth in consumer-facing brands in Europe and North America.

-

Regulation as a Catalyst: Extended Producer Responsibility (EPR) schemes and mandates for recycled content (e.g., in the EU) will accelerate investment in recycling infrastructure.

-

Consolidation & Integration: Leaders will be those who control integrated supply chains—from PX to fiber—and invest in chemical recycling technologies.

-

Innovation in Functionality: Development will focus on enhancing performance (e.g., natural feel, anti-odor, smarter textiles) to justify premium positioning.

Read More-

https://www.zionmarketresearch.com/de/report/steam-turbine-mro-market

https://www.zionmarketresearch.com/de/report/polyeste-fiber-market

https://www.zionmarketresearch.com/de/report/next-generation-packaging-market

https://www.zionmarketresearch.com/de/report/human-insulin-market

https://www.zionmarketresearch.com/de/report/artificial-intelligence-drug-discovery-market

https://www.zionmarketresearch.com/de/report/waterproofing-membrane-market-size

Conclusion

The polyester fiber market stands at a crossroads. Its dominance is undisputed, built on decades of cost and performance advantages. However, its license to operate in the 21st century now depends on its ability to evolve from a linear, fossil-based model to a circular, sustainable one. The companies that will lead the next phase will be those mastering the triple balance of scale, innovation, and sustainability, effectively weaving the future not just of textiles, but of a more circular industrial economy.